A Generation Is Trying to Gamble Its Way Out

On the casino economy, the Cantillon Effect, and how to actually build a life when the default path is dead.

The money is broken. The financial system is rigged. And an entire generation is trying to gamble its way out of the grift of the previous generation.

This is not an accident. It is the predictable outcome of over a century of monetary debasement and we are in the stage now where the consequences are visible to everyone, yet still understood by virtually no one.

The Scale of It

The fastest-growing financial category in America is not savings. It is not investing. It is not even bitcoin or cRyPtO.

It is gambling.

Sports betting was a $1 billion business in 2019. In 2025 it booked $17 billion in revenue on $167 billion in wagers. A 15x scale-up in six years.

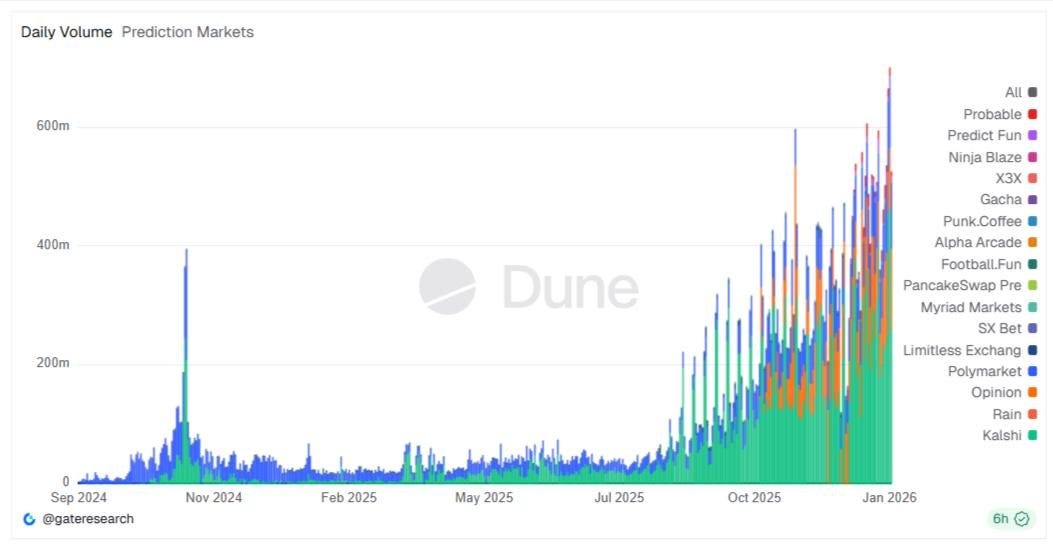

Prediction markets are growing even faster. In November 2024, a single Polymarket contract on the presidential election pulled in $3.7 billion. A cultural phenomenon.

Eighteen months later, that entire year looks like a drop in the bucket. Kalshi and Polymarket have already done $60 billion in combined volume in 2026 alone, more than the entire sector did in all of 2025. Bernstein is forecasting the category hits $1 trillion by 2030.

Kalshi raised $1 billion last month at a $22 billion valuation. Polymarket is now valued at $15 billion. Vlad Tenev, the CEO of Robinhood, calls it the prediction market super cycle. He is right. We are in a super cycle for gambling.

I see it all around me. Most of my friends sports gamble now. More of them are on Polymarket and Kalshi every week. A lot of them already took their shot on memecoins and meme stocks back in 2020 and 2021. With little success, of course.

So why is gambling of every flavor suddenly everywhere?

Who Actually Did This

The easy story is that gambling is just entertainment. A harmless release valve. Or that DraftKings and Polymarket and Robinhood are the villains for building the casinos.

Both stories are wrong. The real villains sit upstream.

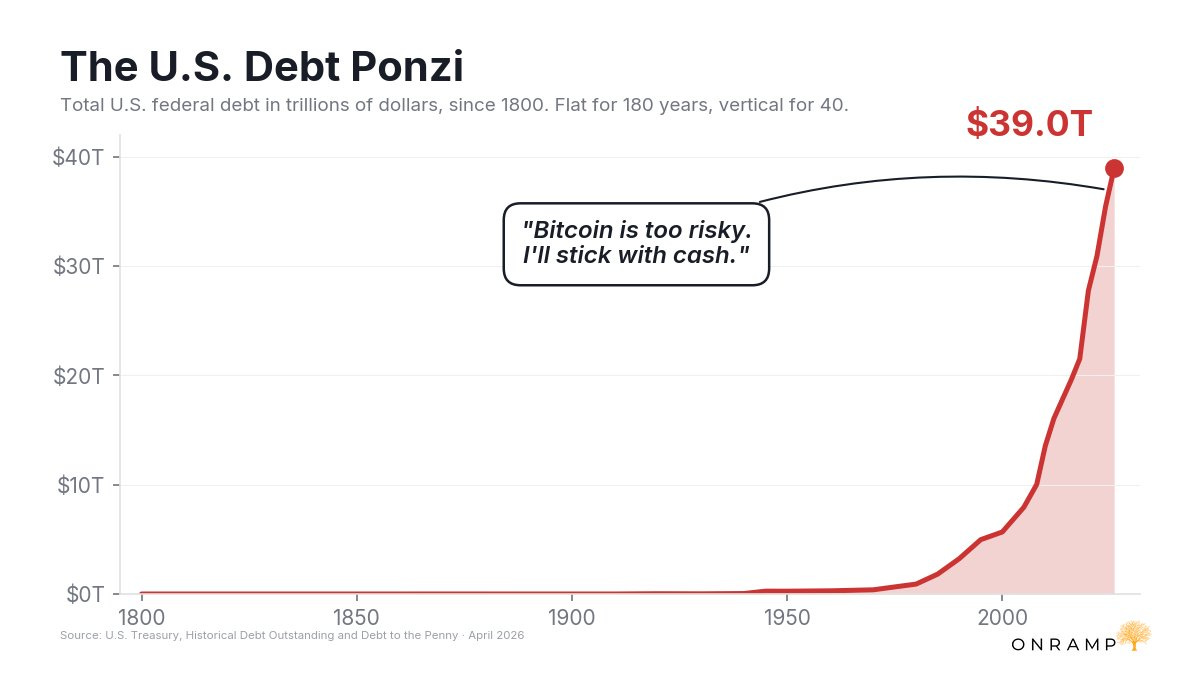

The Federal Reserve, in coordination with the US Government, has been debasing the dollar since 1913. The pace accelerated after 1971 when the last link to gold was severed. It accelerated again after the 2008 financial crisis. It accelerated again after COVID. Every crisis gets the same response. Print. Pump. Repeat.

The project is simple. Print the money. Pump the assets. Spread the consequences across everyone who holds dollars or earns wages. Concentrate the benefits in everyone who already owns assets.

This is not a conspiracy theory. It is the system working as designed.

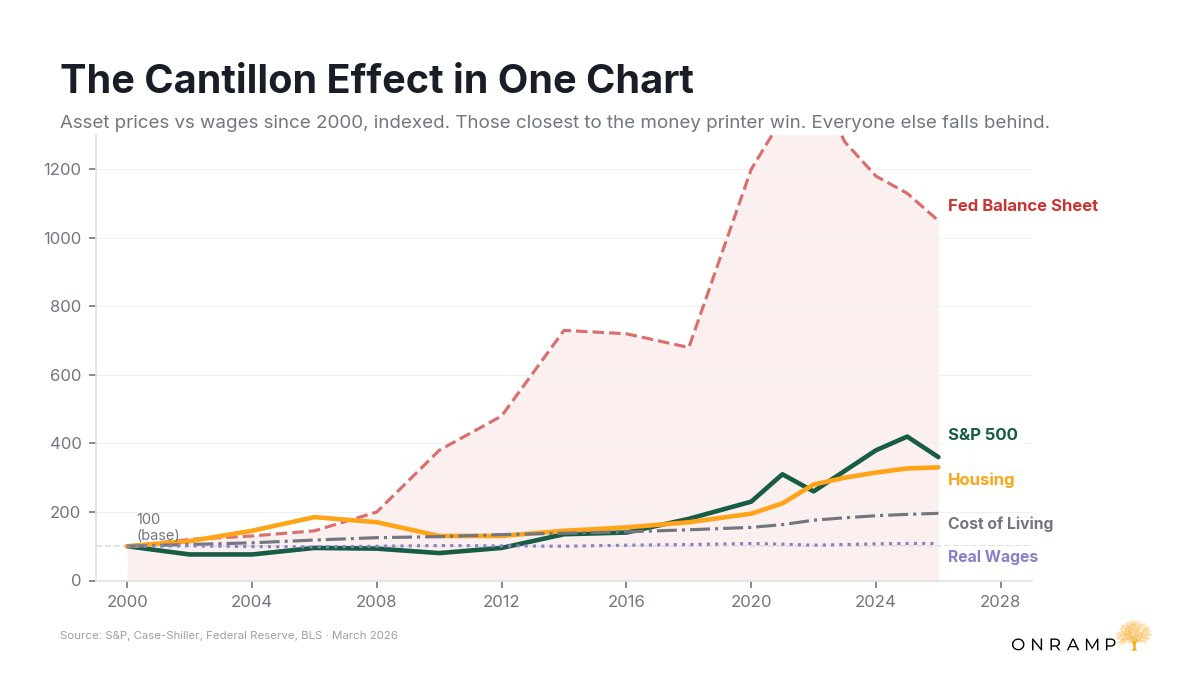

It even has a name. The Cantillon Effect. Named for the 18th-century economist who first described it. New money does not reach the economy uniformly. It reaches the people closest to the money printer first, and they get to spend it before prices adjust. By the time it trickles down to wage earners, the purchasing power is already gone. The insiders buy the assets. Everyone else foots the bill.

That is what has been happening in America for a century. It just got dramatically worse in the last fifty years, and outright grotesque in the last fifteen.

The casinos are downstream of that.

Robinhood did not break the economy. The Fed broke the economy and Robinhood is where people go when they realize the old game is unwinnable. Polymarket is the symptom, not the disease. DraftKings is the symptom, not the disease. Memecoins are the symptom, not the disease.

But the disease is real, and the data is everywhere if you know where to look.

The Evidence

In 1971, a median home cost 2.5x the median income. Today it costs 7x. The most stretched level in US history.

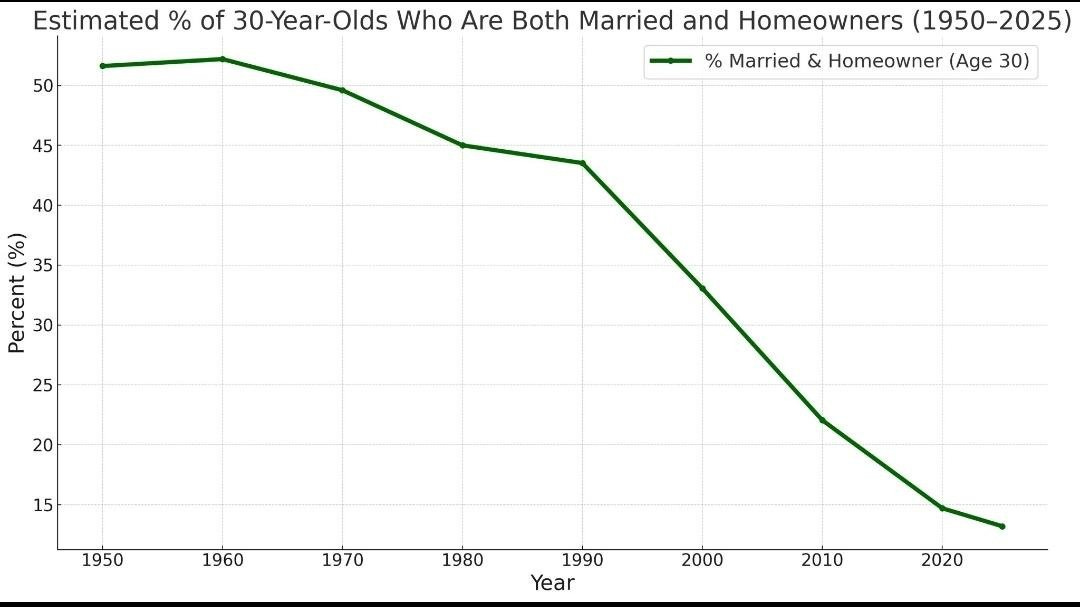

In 1950, more than half of thirty-year-olds were married and owned a home. In 2025, fewer than 15% do.

Wages are up. Prices are up more. The things that actually matter for a middle-class life (housing, healthcare, education, insurance, groceries) are compounding at 10%+ per year. The paycheck gets a 3% bump and everyone is told they’re doing great.

The boomers are sitting on $80 trillion in wealth. Most of that gain came from holding assets while the currency they were priced in got debased. It looked like smart investing. It was actually just being on the right side of the print.

The generation behind them is on the wrong side of it.

If you are 20-40 and looking around, the default path is dead. A corporate job that AI is replacing. Wages that do not keep pace. A 401(k) running a race it cannot win. A house you will never afford at normal savings rates. A retirement planned around assumptions that no longer hold.

So people look around and think: the normal game is unwinnable. Why not swing for the fences?

That is not greed. That is despair dressed up as hope.

And waiting for them on the other side is an industry that has perfected the business of monetizing that despair. Robinhood built a slot machine and called it a brokerage. DraftKings built a casino and called it sports. Polymarket built a casino and called it information. Coinbase built a casino and called it crypto. Memecoins are just the chips. The casinos did not cause the problem. But they are standing there with their hand out, ready to take what little you have left.

What Actually Works

The most unpopular thing you can say in 2026 is that boring still works and that there is still hope.

Save more than you spend. Store your savings in scarce assets that the state cannot dilute. Do it over decades, not weeks.

Nobody wants to hear that. Everyone wants a quick fix. It may not even feel like it’s working, but then one day you look back over the years and realize it is.

As my father has told me, every generation has its challenges. Ours is to figure out how to build against a broken system instead of checking out of it. The easiest thing to do is to check out, gamble, and DOOM.

Beyond just saving, I try to be high agency in a world that is increasingly passive. I try to create opportunity for myself instead of waiting for it. I try to stay on the frontier of new technologies because the frontier is where asymmetric rewards live. I’m using AI every day to do more work in less time, learn faster, and identify where I can be more valuable to my company. I’m also always looking for opportunities to increase my earnings outside of my day job.

Like anyone who understands how broken the circumstances are and what caused them, it can be easy to get discouraged. But I generally keep a positive attitude even when it looks ugly out there. Having a positive outlook on life is incredibly important, especially when others around you are dooming.

Focus on what you can control. Tune out what you can’t. Spend your time trying to improve your abilities instead of watching others.

Don’t hyper-gamble. Don’t trade shitcoins. Tune out the prediction markets.

It’s a long game. The playbook is older than any of us. Spend less than you make. Save in scarce assets. Work hard. Stay optimistic. Compound.

It’s harder in the circumstances we find ourselves in today. But that is still the playbook. And it still works.

One Last Thing

The fastest-growing financial category in America is gambling. That should tell you something about where we are.

The way out is not another bet.

It is sound money. Held the right way. For long enough.

Paired with agency. And the willingness to build.

Don’t gamble your way out. Build your way out. NEVER DOOM.

The gambling stuff is bonkers…

Amazing how the solution is timeless regardless what’s the hype de jour. And thankfully we have the best version of that timeless solution we’ve ever had.