Stocks Crash or the Dollar Does. Either Way, Bitcoin Wins.

Paul Tudor Jones gave the bears their stock crash thesis and the bulls their Bitcoin endorsement. They're the same call.

Two of Paul Tudor Jones’s takes from his viral interview this week are getting clipped everywhere. The bulls are grabbing the Bitcoin one. The bears are grabbing the stock one. They’re missing that it’s the same call.

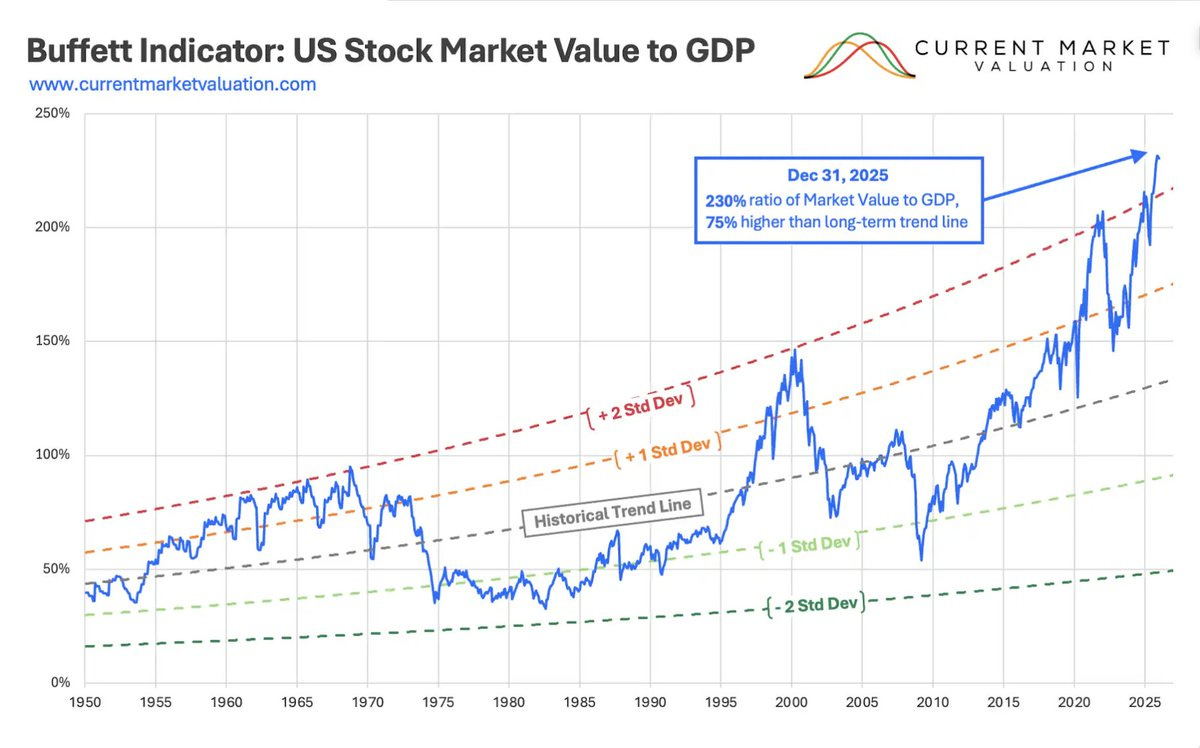

PTJ said US equities are the most leveraged they have ever been, with a market cap to GDP ratio of 252%. He also said Bitcoin is “unequivocally the best inflation hedge there is, more than gold,” because it’s finite.

The connection is the whole story. There are only two paths from where we are. Stocks correct hard, which forces the Fed back to the printer to save the system. Or the printer keeps running to prevent the correction in the first place.

Both paths debase the dollar. Both paths lead to Bitcoin.

The bubble call is not new

PTJ didn’t explicitly call the stock market a bubble, but he did point to the data. He compared market cap to GDP across the major historical crashes:

1929: 65%

1987: 90%

2000: 170%

Today: 252%

Again, PTJ doesn’t call this a bubble. He warns valuations are stretched.

That warning isn’t new. Plenty of investors have been calling this market a bubble since the early days of QE close to two decades ago. Many smart fund managers and market commentators have been making this call for fifteen years.

If retail investors had listened, they would have been out of US equities for the entire post-GFC bull market.

Here’s what that would have cost them. The S&P 500 has returned roughly 10x since the March 2009 low, with dividends reinvested. About 14.5% per year. The Nasdaq has done significantly better. Sitting in cash waiting for a mean reversion that hasn’t come is the most expensive macro call retail investors keep making.

From every fundamental metric, yes, the market is overstretched. But it’s hard to say how it all resolves, because the system cannot afford a real correction without a significant reworking of the global financial system.

The system can’t afford a real correction

This is the part PTJ hints at but doesn’t quite spell out.

Consider what a 30% S&P drawdown actually does in 2026.

Capital gains revenue is about 10% of federal receipts. It collapses. The deficit, already running at $2T+ annually, blows out further.

Public and private pensions chasing 7% return assumptions get crushed. That has massive downstream effects for everyone relying on those pensions for retirement.

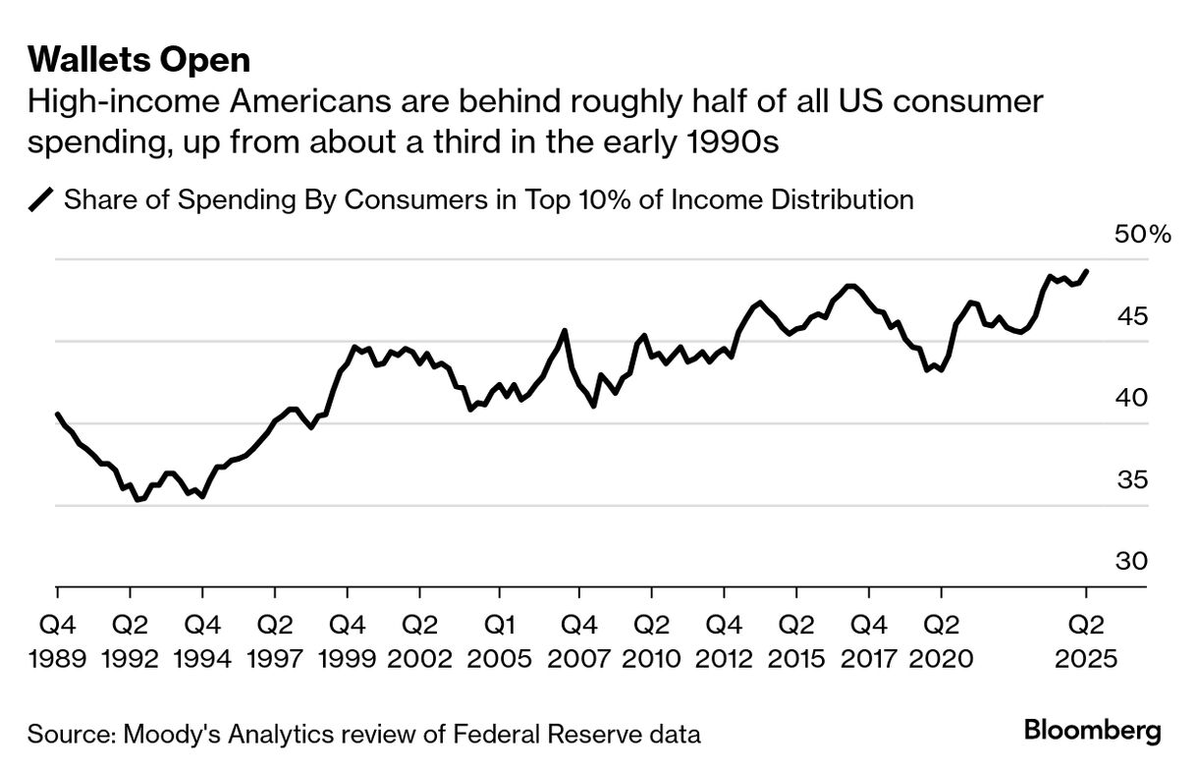

Then there’s the wealth effect. Per Moody’s analysis of Federal Reserve data, the top 10% of earners now account for about 49% of all US consumer spending, the highest concentration on record.

That spending is driven almost entirely by financial asset inflation. When stocks and home prices go up, this cohort spends. When they go down, they pull back. The whole consumer economy is running on the wealth effect of a small group of people. And mind you, US GDP is about two-thirds consumer spending.

Meanwhile we sit on $39 trillion of federal debt with interest expense eating a record share of receipts. If you let the consumer economy collapse and you let the market collapse, you’re also weakening demand for US Treasuries. If tax receipts are collapsing, how do you make good on those obligations? You don’t. That’s a debt spiral.

A 30% drawdown in equities in 2026 doesn’t just hit portfolios. It blows out the budget, breaks pensions, kills consumer spending, and forces the Fed back to the printer.

The path through is more debasement.

Bessent and Warsh are setting the table

PTJ called Bitcoin the fastest horse in 2020 because of the fiscal and monetary impulse. He went looking for the asset most exposed to dollar debasement. Bitcoin won on a finite-supply basis. He bought it. He was right.

The setup has been quiet for the past few years. The Fed delivered the fastest rate hike in history.

But look at what’s loading right now. Bessent calling the shots at Treasury. Warsh teeing up rate cuts. In his Senate confirmation answers, Warsh suggested using “trimmed mean” inflation, which currently prints meaningfully lower than headline CPI. Translation: change the metric, justify the cuts. We’re watching them set up the cover story for accommodative policy in real time. I actually missed that detail until I saw Larry Lepard point it out (here is the post).

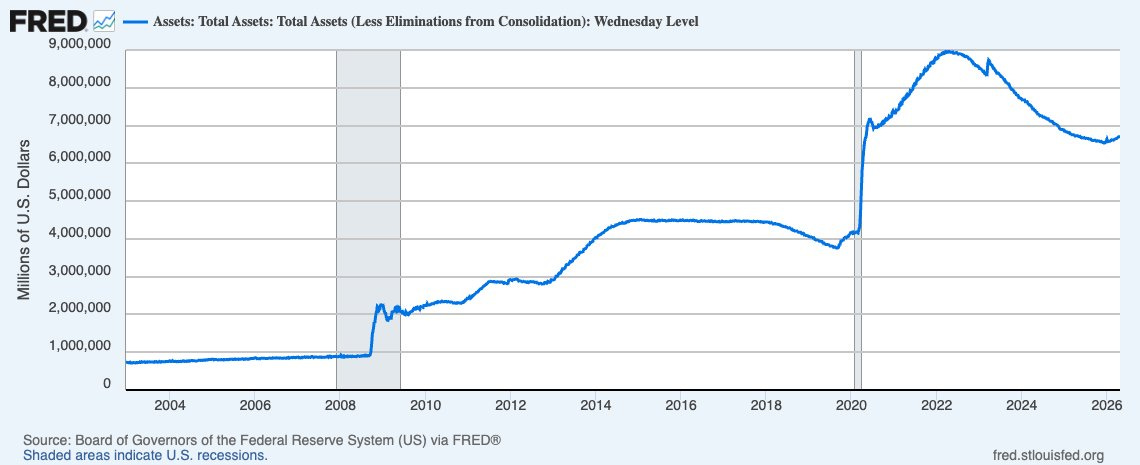

Lepard’s Big Print framework is worth holding next to all of this:

Big Print 1 (GFC): $3.6T

Big Print 2 (COVID): $5.0T

Big Print 3: loading

Lepard wouldn’t be surprised by an unscheduled Fed meeting after May 15 and a 100 bps cut. That’s before any new “crisis” forces their hand.

The setup that made Bitcoin the fastest horse in 2020 is reassembling. Most people aren’t paying attention. By the time they are, they’ll have missed the prime opportunity.

The trader-investor distinction matters

This is the most important part for me, and the part most people will gloss over.

Paul Tudor Jones is one of the greatest traders to ever live. He has a 50-year track record. His fund has a -0.12 correlation to the S&P 500. He makes money from trading. Almost nobody listening to that interview has his instincts, his information edge, or his risk discipline.

I am not a trader. I would lose money if I tried. I’m honest with myself about that.

I earn money by working at a business. Bitcoin is my savings.

Most people listening to PTJ are in the same position I’m in. They earn from a job or a business they own. They are looking for somewhere to store the wealth they’ve built without watching it get inflated away. They are not looking to time markets.

For us, the right takeaway from a PTJ interview isn’t to start trading. It’s to ask which asset best protects the value of work in a system designed to debase it.

In this interview, PTJ admitted he was wrong about Warren Buffett. For decades he railed on Buffett as someone who got lucky in a long American bull market. After listening to the Acquired podcast on Berkshire Hathaway, he changed his mind. Now he calls Buffett the real genius. Compound interest is the actual game. Trading is an attempt to capture alpha around the edges.

He also said Bitcoin is the best inflation hedge there is.

Hold the asset that compounds via increasing scarcity in a fiat system that compounds via decreasing scarcity. Don’t trade it. Don’t time it. Just hold it.

PTJ won’t say it that simply. He has 50 employees and a fund to run. But you can read between the lines.

What I’m actually doing

Same thing I have been doing. Holding Bitcoin. Continuing to DCA. Keeping cold storage tight.

Most of my net worth is in Bitcoin. I’ve said that publicly many times. I’m not adding leverage. I’m not selling on dips. I’m not changing my thesis because PTJ thinks stocks are overvalued, and I’m not trading because Lepard expects Big Print 3.

I am paying attention to the catalysts. PTJ talked about looking for “catalytic moments” where something undervalued, underowned, and off-sides finally has a reason to move. Bitcoin sits at the intersection of all three in a world where the only path through fiscal dominance is debasement.

The bubble call and the Bitcoin call are not separate calls. They’re the same call. You can decide if you want to hear it.

If this resonated, please leave a “like” and share with one person who would benefit from reading. Also I welcome any comments or questions below.

The PTJ synthesis here is right. His stock bubble call and his Bitcoin call aren't in tension — they're the same logical conclusion wearing different clothes. The only variable is the timing and mechanism of the debasement. The Warsh/trimmed-mean point is the most underreported angle. If the Fed adopts a new inflation metric that prints consistently lower than CPI, you've functionally cut rates without touching the stated rate. That's the cover story being assembled in real time. The DCA/cold storage/no leverage approach is where I've landed too after running the numbers. The traders will time better entries. The long-term holders will hold through volatility. Both work for different people. The ones who lose are the ones who do neither — panic buying highs, selling dips. I covered the Big Print thesis and what it means for BTC positioning in my last issue at Beyond The Coin. Same conclusion: the setup from 2020 is reassembling. Most people aren't paying attention yet.