The Wealth Gap, Explained

It's not capitalism. It's broken money.

The Wall Street Journal just published a piece about the explosion of ultra-wealthy households in the US. It presents the data of how wealth demographics have shifted dramatically in favor of the ultra wealthy over the past several decades.

The exploration of “why” this is happening is incredibly surface level, touting rising stock prices, home values, and private business valuations.

But the article misses the most important part. It never explains the root cause of why this is happening. And it’s a critical point to consider, especially in the context of rising support for wealth taxes, universal basic income, and other redistributive policies gaining traction in the United States.

I’ll do my best to explain why this is happening. But before I do, I’d like to share some staggering numbers from the article.

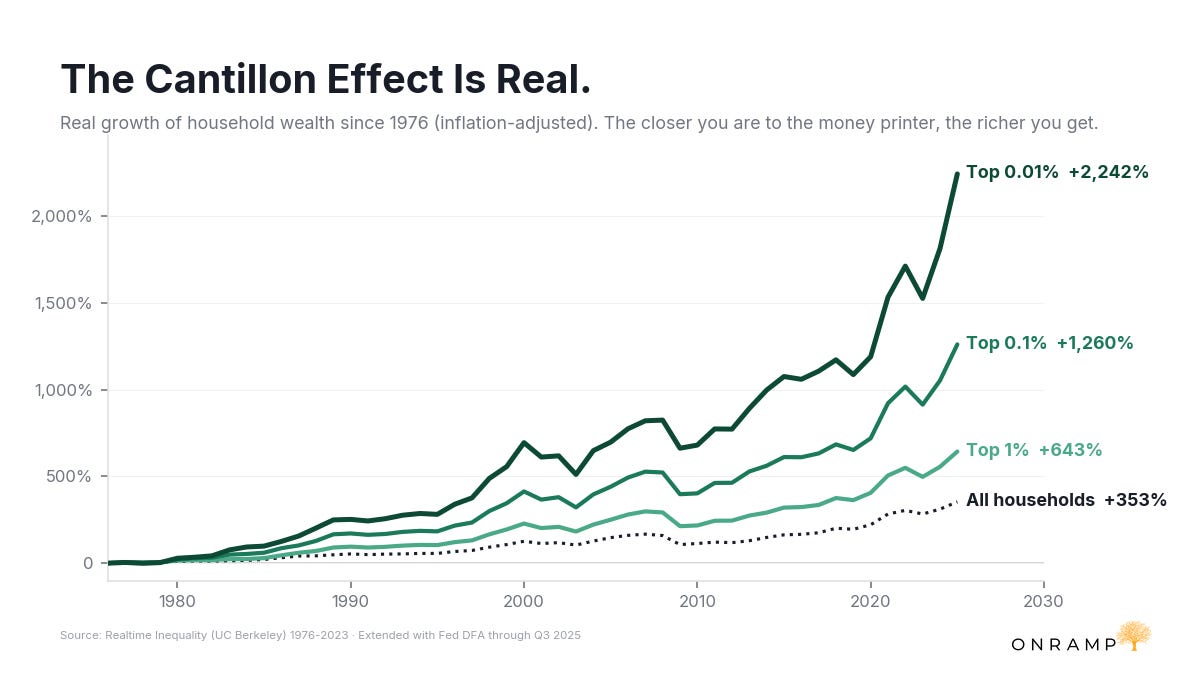

The top 0.1% of households have seen their wealth grow over 13x in the past 50 years, adjusted for inflation. 430,000 US households are now worth $30 million or more. 74,000 are worth over $100 million. Those numbers have exploded in recent decades, far outpacing population growth.

Meanwhile, the bottom 50% of American households had negative average net worth from the mid-1990s through the start of COVID. Negative. It took stimulus checks and rising home values just to bring it back above zero.

It shouldn’t surprise anyone at this point that people are calling for massive wealth redistribution. And I actually understand why. I don’t support these policies, but I can understand why they’re gaining support. The wealth inequality in this country is incredibly problematic, and it is not a product of a free capital market. It’s a product of broken money.

The Wealth Gap, Explained

The WSJ notes that “for the top 0.1%, nearly 72% of their wealth is made up of corporate equities, mutual fund shares and private businesses. The S&P 500 has more than tripled in the past decade.”

I think this is an incredibly important data point, because anyone who reads it should ask the obvious question. Why has the S&P 500 tripled in the past decade? What is actually driving that?

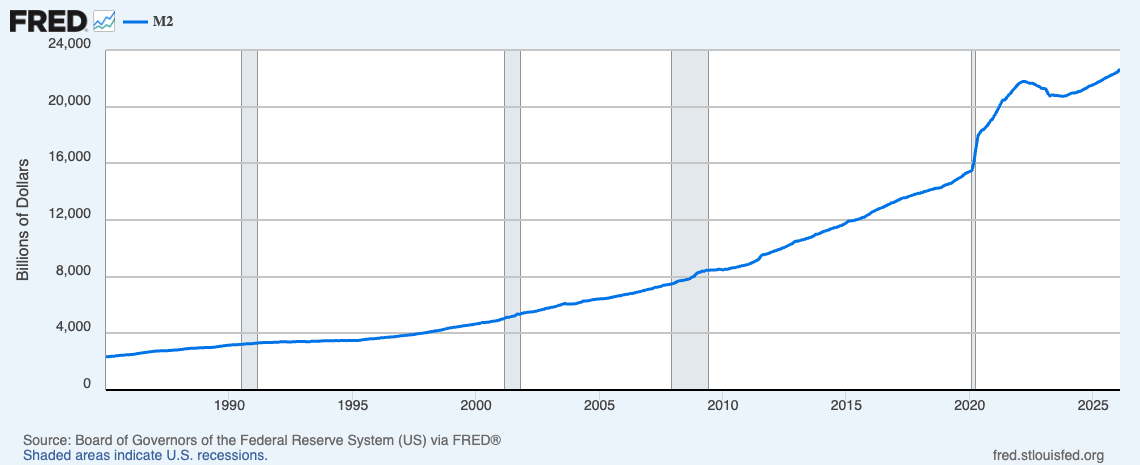

Look at these two charts. The first is M2 money supply, which is a measure of the total number of dollars in the US financial system. The second is the S&P 500 over the same time period.

Notice anything? They tell the same story. More dollars, higher asset prices.

Look at the acceleration after 2008. Look at the vertical spike in 2020. The M2 chart shows roughly $6 trillion in new dollars created in less than two years. The S&P chart shows the stock market nearly doubling over that same stretch. That is not a coincidence.

The stock market is not going up because the economy is that much more productive. It’s going up because trillions of new dollars are being created and they have to go somewhere. They flow into financial assets. Stocks, real estate, private businesses. And the people who already owned those assets get wealthier automatically while everyone else pays higher prices for everything from groceries to rent to insurance.

This is the mechanism behind the wealth divide. The Federal Reserve creates new money to bail out the financial system, to keep interest rates low, to finance government deficits. They dropped interest rates to zero after 2008 and kept them there for over a decade. Then in 2020 it happened again on an even larger scale. Each time, asset prices surge. Each time, the gap widens.

For the average person, here is what this means in simple terms. When more dollars are created, the dollars you already have buy less. But the assets that absorb those new dollars, stocks, real estate, businesses, go up in price. If you own those assets, your wealth grows. If you don’t, your cost of living rises while your savings lose value.

This process has a name. It’s called the Cantillon Effect, named after an 18th century economist who observed that when new money enters an economy, it doesn’t reach everyone at the same time. Whoever gets it first benefits the most.

Here’s how it works today. New money flows first to the financial system, to banks, to large institutions, to well-connected borrowers. They invest and expand at today’s prices before those prices adjust. Asset prices rise as all that new money chases a limited number of assets. Consumer prices follow. And wages? Wages rise last, usually well after purchasing power has already declined.

The result is a wealth transfer that most people can feel but can’t quite explain. Your groceries cost more. Your rent is higher. Your insurance premiums jumped. But the stock market tripled. The people closest to the money printer got richer. Everyone else got poorer.

This is not a conspiracy theory. It’s a well-documented monetary phenomenon. And it has been the primary driver of wealth concentration in the United States for decades.

The Generational Divide Is Staggering

I think we can all agree that if the economy doesn’t serve younger people and doesn’t help them get ahead in life, that is a fundamental problem. They are the future of this country.

And what you’re seeing now is more and more younger people checking out. They feel like they have no shot at a future, so why build one? It’s easier to open up an account to gamble on sports or prediction markets. It’s easier to just check out entirely than it is to face the seemingly insurmountable task of meeting the standard of living your parents had.

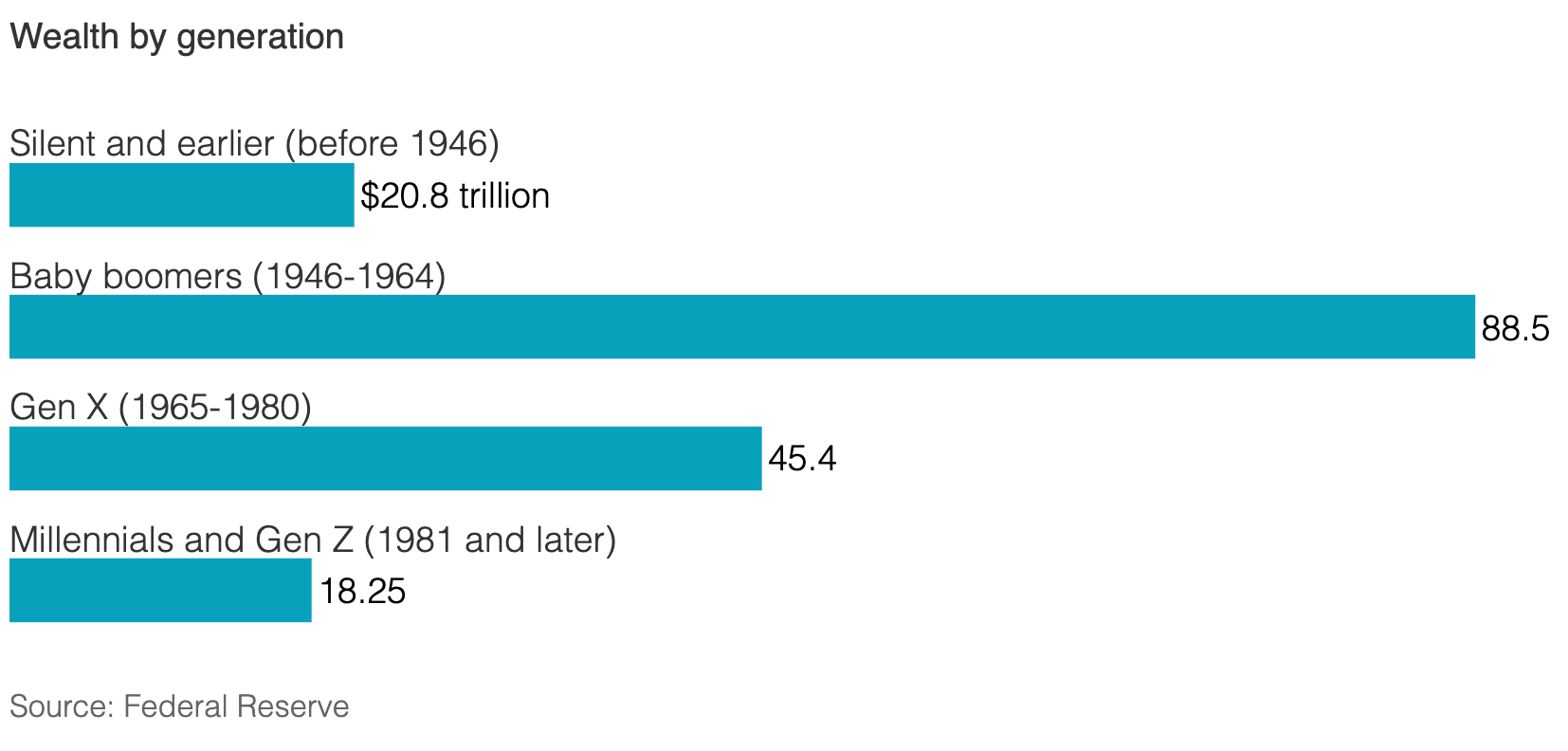

The article points out a massive generational divide. Baby boomers collectively hold $88.5 trillion. Millennials and Gen Z combined hold $18.25 trillion. Two thirds of the households worth $30 million or more are headed by boomers.

I don’t say this to blame the boomers. Many of them worked hard and made great decisions. But they also had the wind at their backs in a way that younger generations simply do not.

They started accumulating assets decades ago. They bought their first homes when housing was still affordable. And they rode the wave of declining interest rates from the highs of 1980 all the way down to nearly zero for the past decade plus. All asset prices appreciated meaningfully under that tailwind of lower rates and more dollars entering the system.

Now you can kind of see that this is broken. The median homebuyer today is 59 years old. In 2010 it was 39. The median home price is now above 7x median income. That’s worse than before the Great Financial Crisis. I experience this firsthand, like almost everyone in my peer group. It’s just expensive to be alive.

The wealth gap isn’t an accident. It’s the predictable, mathematical outcome of a system that inflates asset prices while wages stagnate. If you already own the house, the stocks, the business, you get richer. If you’re still trying to get in, the door moves further away every year.

The Frustration Is Valid. The Proposed Solutions Aren’t.

I completely understand why people are calling for wealth taxes and universal basic income. The frustration is real. People can feel that the system is broken even though most do not know the exact reason why.

But these proposals treat the symptom, not the cause. A wealth tax doesn’t change the fact that money creation benefits asset holders. UBI doesn’t change the fact that every new dollar printed reduces the purchasing power of the dollars people already have. You can’t solve an inflation problem with more inflation. Redistributing newly printed money doesn’t fix anything if the money itself is losing value. And I’m sure in the process the government would find a way to line their own pockets handsomely.

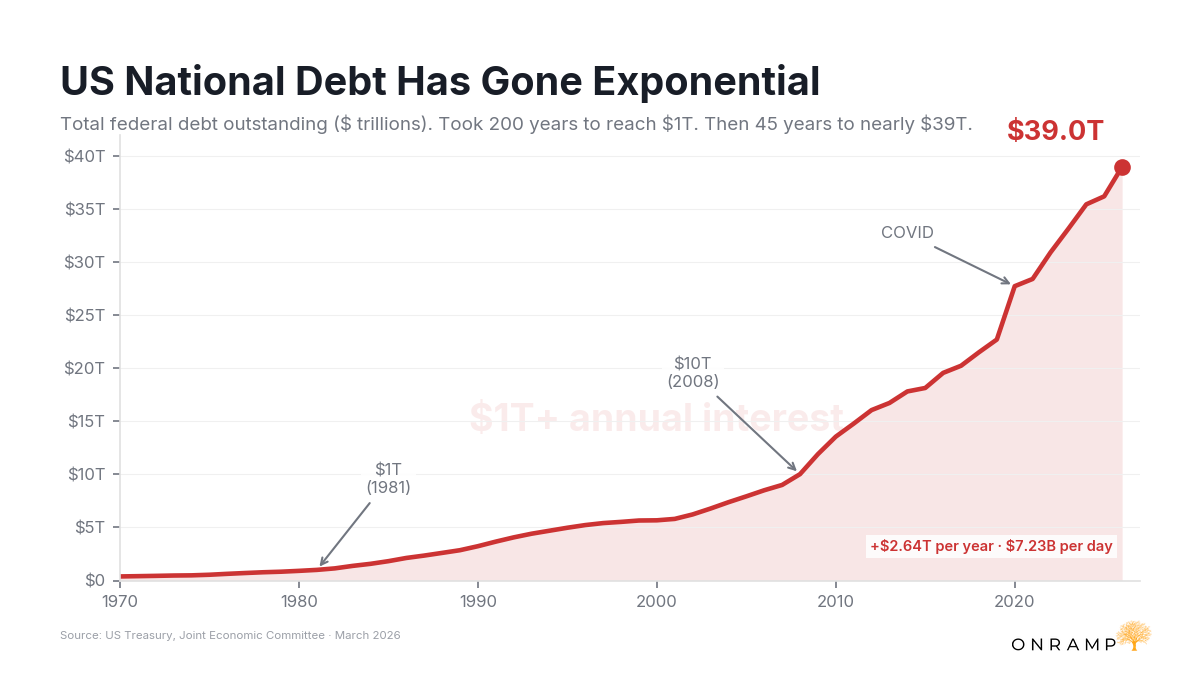

Since 1971, every financial crisis has been met with the same playbook. Lower rates. Print money. Bail out the system. Each time, the gap widens. Each time, the people at the bottom fall further behind. And each time, the proposed fix is some variation of “let’s do more of the thing that caused the problem.”

The US has $39 trillion in federal debt. The dollar has lost 97% of its purchasing power since 1913. There is no political path out of this that doesn’t involve the printer. Both parties are responsible. Neither will stop spending. The only exit is more money creation, which means more wealth concentration, which means more frustration, which means more calls for redistribution. It’s a cycle, and it’s accelerating.

What I’m Actually Doing About It

I’m not going to pretend I have the answer for fixing this system. I don’t. But I do know what I’m doing about it in my own life, and I’ll share my reasoning.

First, I’m focused on earning aggressively. If your income isn’t growing at 10 to 15% per year, you’re losing ground in real terms. That’s a tough reality. The thing that secures my family’s future isn’t any single asset, it’s my ability to earn. I’m all in on bitcoin but I’m not banking on it to save me. It’s possible that bitcoin could go to zero, although the trend moves further in the other direction every day. What I’m trying to figure out right now is how to stack several incomes. The good news is that AI is creating efficiencies that were previously unimaginable.

Second, I save in scarce assets. I use bitcoin as my primary savings vehicle because it can’t be debased. It has a fixed supply of 21 million. No government, no company, no person can print more of it. In a world where the only exit is more money creation, I want my savings in something that doesn’t lose value every time a central banker fires up the printer. Bitcoin’s 5-year return looks rough right now, but the 3-year and 6-year crush every other asset class. This is why dollar cost averaging is your best friend.

Third, I’m building locally. I write this newsletter every week, but I’ve also launched a local community to bring together others who think like me. I believe in the power of local networks and the compounding effect of surrounding yourself with people who are building rather than complaining.

The Sound Life Framework

You can’t fix the monetary system. But you can build a life that isn’t entirely dependent on it.

That means earning more than you think you need to. Saving in things that can’t be diluted. Building skills and relationships and projects that compound over time. Being intentional about where your time and energy go instead of doom scrolling about how unfair it all is.

The WSJ data is shocking, but it shouldn’t be surprising. This is what happens when money is broken. The people who own assets get richer. The people who don’t get poorer. It’s been happening in this country for decades and it’s accelerating.

The question isn’t whether the system is rigged. The data makes that clear. The question is what you’re going to do about it in your own life.

I know what I’m doing. I’m earning, saving in bitcoin, building every week, and trying to live well despite a system that makes it harder every year. That’s the sound life.

If this piece helped you understand what’s actually going on, share it with someone who needs to read it. I write one of these every week. Make sure you’re on the list so you don’t miss the next one. And if you reply or comment below with what you thought, it helps me keep improving.